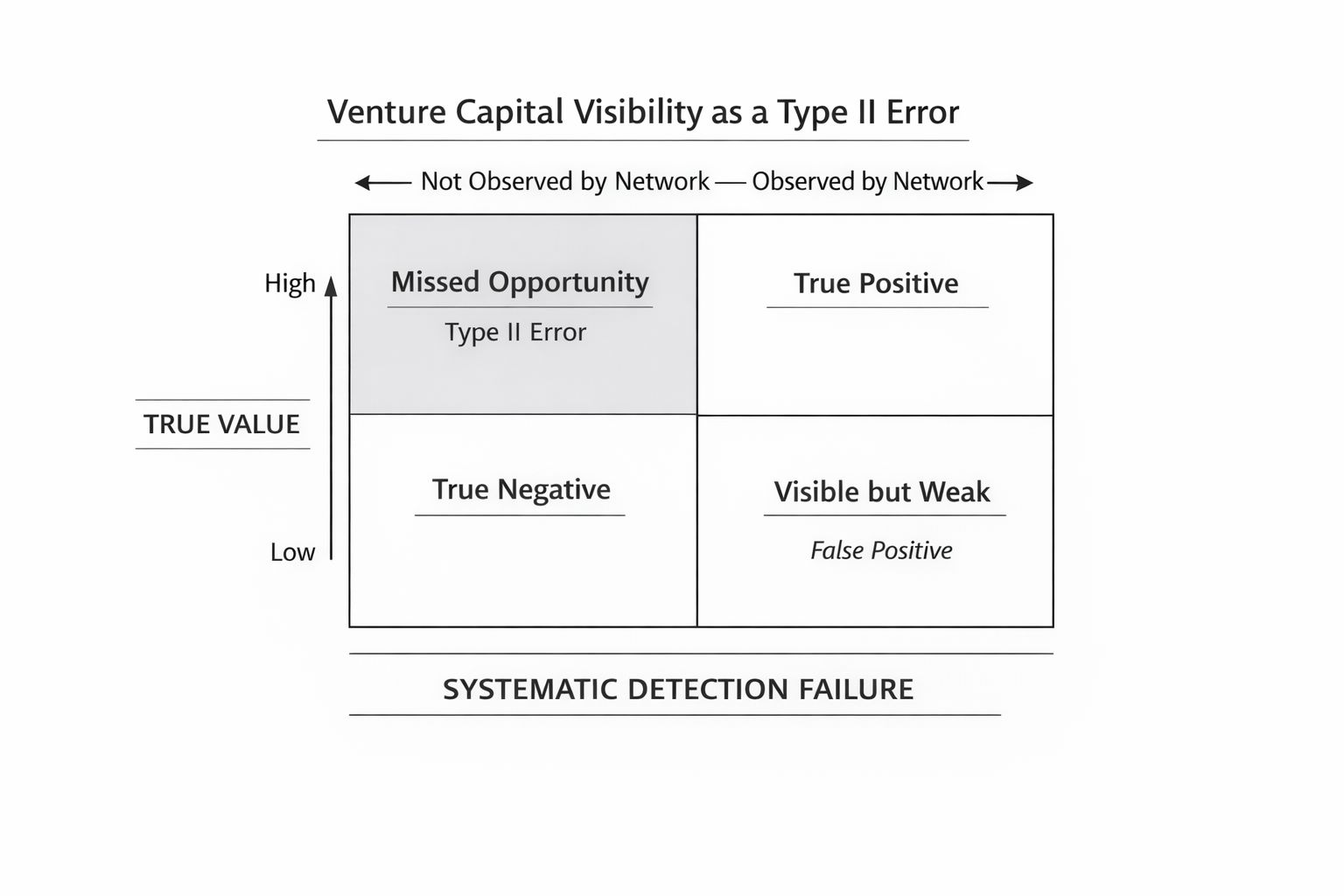

Signal over noise: solving the venture capital visibility problem

The venture capital market, shaped by US norms, has a persistent inefficiency: capital allocation is not a function of the highest risk-adjusted returns, but of the most observable ones within a tight, relationship-based network. This is not a ‘discovery deficit’, a diagnosis that implies mere search friction. For startups building outside San Francisco and New York, this creates a systematic detection failure known as a Type II error, the statistical term for when something valuable gets missed entirely.

While founders with the right market connections tend to secure capital on relationship strength and warm introductions, teams with stronger execution in emerging markets face invisibility. So, stop trying to penetrate the network through conventional means. Instead, publish an evidence base that can be assessed independently of personal networks. Make it effortless for investors to evaluate your business until the results speak for themselves.

The referral architecture and its selection bias

Venture sourcing favours founders with the right connections over those with stronger fundamentals. This creates a systematic selection bias where warm introduction culture generates false negatives for outsiders. Consider an emerging-market startup outside elite networks with 150% net revenue retention and a 0.3x burn multiple (the amount spent to generate each incremental dollar of annual recurring revenue) struggling to secure meetings, while a Stanford team in the United States with 60% retention and a 3x burn multiple closes an oversubscribed round in weeks. The difference isn’t merit – its network position acting as a rough proxy for quality.

Your venture remains invisible not because your metrics are weak, but because they’re invisible to the network’s discovery mechanisms. Network-connected teams with weaker fundamentals secure capital access simply because they exist ‘in the flow’ of investor deal sourcing.

However, this asymmetry embeds a hidden leverage mechanism: time arbitrage. While you remain undetected by the hype cycle, you retain a longer, quieter window to compound operational leverage and strengthen fundamentals before the broader market attempts to price you in. Bay Area competitors must allocate resources toward network cultivation from inception, eating into execution time. You can optimise purely for operati

onal compounding. The network’s blind spot becomes strategic depth – if you understand how to exploit it.

The filter: what systematic diligence actually measures

When storytelling fades and pitch narratives are set aside, investors look at three things.

First, categorical precision. Investors face attention constraints when processing deal flow. If they cannot quickly classify your business model and competitive positioning within thirty seconds, evaluation terminates. This is not arbitrary – it reflects how pattern recognition operates under cognitive load. You must trigger their pattern-matching instincts immediately: “We are X for Y market using Z mechanism”. Ambiguity is not intriguing; it is rather disqualifying.

Second, unit economics and growth momentum. Investors

scrutinise burn multiples, sales efficiency ratios, and gross retention to determine whether you have built a scalable engine or a cash-consumptive illusion. But they are not evaluating your current ARR (Annual Recurring Revenue, the predictable subscription revenue stream) – they are evaluating whether your business operates in a compounding or linear regime. This appears in accelerating cohort retention curves that prove increasing product value over time, improving sales velocity showing decreasing customer acquisition costs at scale, and expanding annual contract values within existing customer bases. Venture capital funds exponential growth curves, not steady linear progress.

Third, team verification. Investors bet on track records of execution under uncertainty. This requires empirical evidence: open-source contributions showing technical craft, previous exits proving shipping capability under resource constraints, or domain expertise so deep it reveals itself in architectural decisions rather than pitch deck assertions. They are assessing whether this team can navigate the next three inflection points, not whether they like you.

The strategic response: from network cultivation to informational transparency

The optimal response operates on three principles. First, document everything. Publish architectural decision records explaining technical choices. Ship weekly operational dashboards with metrics on cohort retention, burn efficiency, and sales velocity. Maintain public-facing analytics that answer standard diligence questions pre-emptively. You are not creating content marketing – you are building an evidence base that allows investors to evaluate your venture with minimal extra work.

Second, make your execution discipline publicly observable. This means GitHub repositories with real commit histories, technical blog posts demonstrating architectural sophistication, customer case studies (anonymised if necessary), and public roadmaps showing product velocity. Each artifact reduces the perceived risk of investing in an unknown entity. These outputs make your operational discipline and team capabilities verifiable without requiring investor meetings, enabling rapid benchmarking against the top 25% of startups in your category.

Third, exploit geographic cost differentials. A $2 mi

llion seed round in Warsaw, Jakarta, or Nairobi delivers 2-2.5x the operational runway of identical capital deployed in San Francisco. This is not a consolation prize – it is a strategic multiplier. The arithmetic is straightforward: if Bay Area startups raise Series A at $1.5M ARR with 18 months of runway, use your geographic cost advantage to reach $3M ARR on the same seed capital. You are not ‘catching up’ – you are using differential cost structures to outperform when you enter institutional fundraising markets.

One critical implication: abandon stealth mode. Stealth works for founders with pre-existing network access. For everyone else, opacity is counterproductive. Every week in stealth is a week you fail to accumulate demonstrable proof of execution. Your strategy must be radical transparency – not revealing proprietary algorithms but making execution discipline publicly auditable.

Anti-patterns: why high-potential ventures fail

Ambiguity is the primary failure mode. If an investor cannot categorise your business model and market position in thirty seconds, evaluation ends. This is not a storytelling failure – it is a categorical one. Clarity dominates cleverness in capital markets.

Growth quality failures take two forms. Metric inconsistency – where burn multiple improves while sales efficiency degrades – signals a system not yet under deterministic control. The linear trap – steady 20% month-over-month growth without accelerating cohort expansion or improving unit economics – reveals a services business, not a venture-scale asset.

If you can’t show proof, you won’t get trust Claims of technical sophistication without GitHub repositories, technical blog posts, or architectural documentation ask investors to underwrite faith. Claims of market expertise without customer references or domain-specific thought leadership produce the same result. Investors simply decline these opportunities.

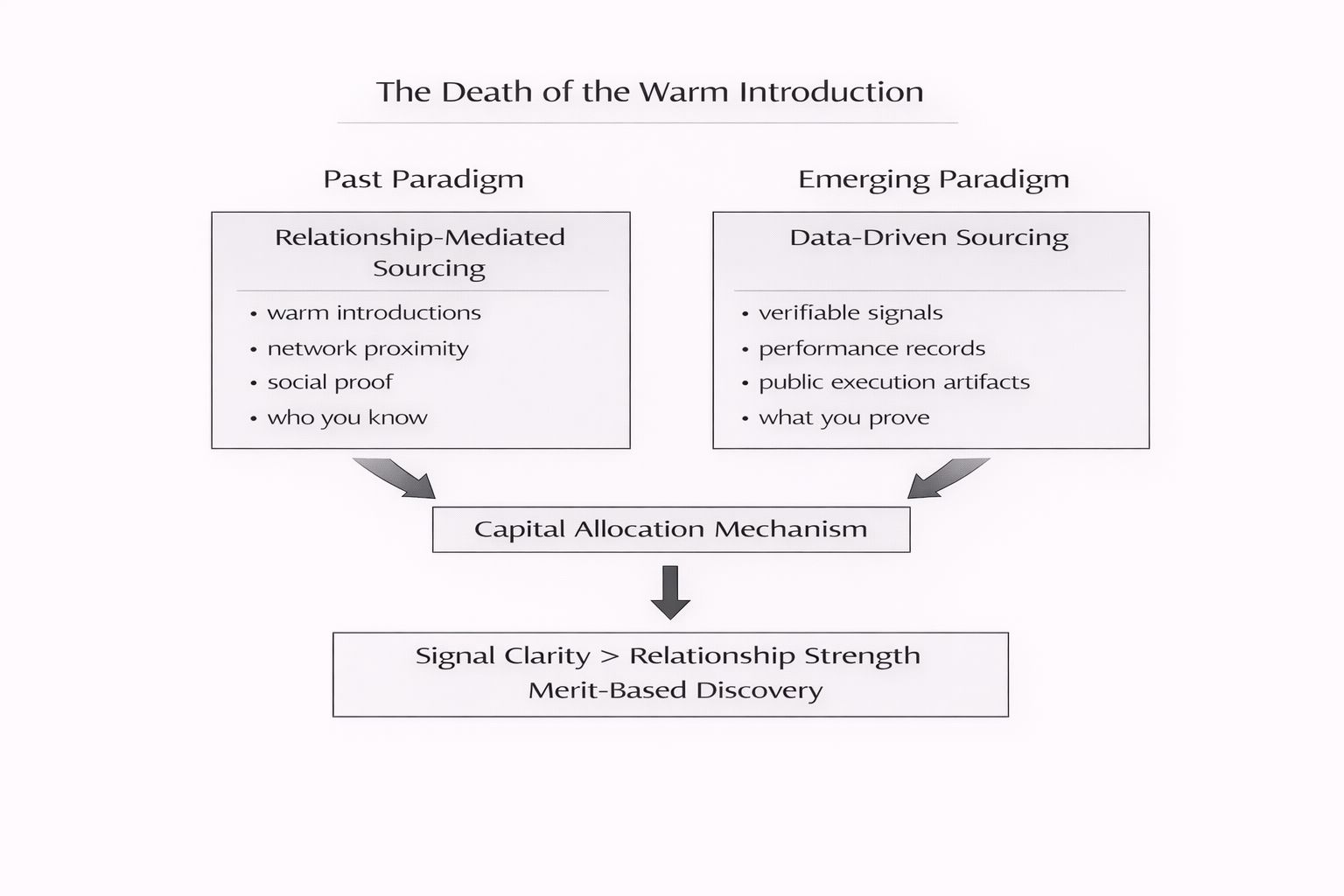

The death of the warm introduction

We are witnessing a fundamental shift in capital allocation from relationship-mediated sourcing to data-driven sourcing. This transition creates substantial advantage for founders who can build merit-based, verifiable signals rather than relying on soci

al proximity. The ‘who you know’ premium is shrinking, while the ‘what you prove’ premium is rising.

For high-quality startups outside major hubs, this opens a practical window to compete strictly on measurable performance. The network moat that historically protected incumbent geographies is eroding. As data-driven discovery becomes universal, capital flows will increasingly align with signal clarity rather than relationship strength.

This arbitrage opportunity exists today but will not persist indefinitely. Once the transition completes, first-mover advantages will accrue to those who built verification infrastructure early. Build performance records compelling enough that investors find you. Founders who reduce evaluation costs until their quality is hard to ignore will capture outsized value. Those who hesitate will remain invisible.