Real Life not Unicorns: Venture Debt and Growth Funding

Not because they are not a sound investment opportunity, but because they do not fit into the VC business model of large investments and super normal returns. For the VC investment model to work, they must target investment opportunities that they believe will achieve at least five times return on investment over three to five years.

As VC Funds grow in scale they need to make larger and larger investments. Few will consider an investment of less than £5m and for many it needs to be nearer £10m. This development has magnified the “funding gap” between companies. Many growth companies do not necessarily need large investments of over £5m. Investment of this scale can distort commercial judgement and lead to risky business strategies to achieve the growth targets VC investment demands, often at the expense of long-term sustainability. The other side of the problem is that private equity investors in private companies often struggle to get their money back; waiting in vain for an exit. How do you develop an investment approach that rewards growth whilst valuing long term sustainability? How do you bridge the funding gaps? How can investors exit in a timely fashion?

Venture Debt offers a solution to providing growth capital to companies while earning a good potential return to investors with a degree of liquidity.

The Venture Capital Business Model

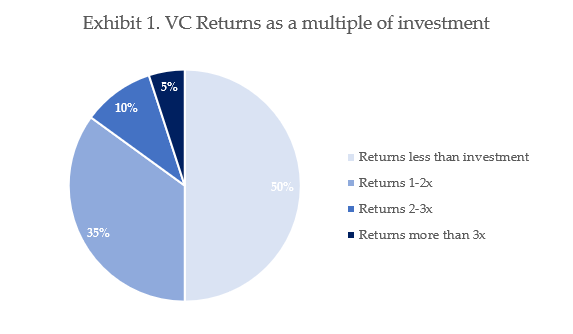

The Pareto Distribution Principle applies to VC investment returns i.e. 80% of returns come from 20% of investments. The analysis in TechCrunch [1] illustrated by exhibit 1 reveals: 5% of investments achieve more than three times investment return; 10% achieves two to three times return; 35% yield 1-2 times returns; while 50% of investment is effectively written off.

Limited partners investors in VC funds such as family offices, institutions, pension funds etc – expect at least a 3x return on capital over the life of the fund (which is typically 10 years). This equates to an Internal Rate of Return (IRR) of 12%. The implication of this is that each investment must have a target IRR of at least 60%. This significantly constrains the range of businesses that can be invested in and causes investment to be focused on a narrow range of sectors and ownership models.

VC’s tend to fall into two categories: Tier 1 are the Kleiner Perkins of this world who are seeking to invest a minimum of £100 million in any one company. Their investments tend to fall into three categories:

- The Unicorn: This is the company that will be worth more than a £1bn within the foreseeable future i.e. 3-5 years. These companies tend to take a disproportionate amount of the total investible funds available

- The may be Unicorn: This is the holy grail ‘one under the radar’ that no-one else has discovered: A game changing disrupter in a huge market. These will take most time and effort from the VC management.

- The “living dead”. These were one time may be Unicorns who have failed to make the grade.

Away from the rarefied heights of unicorn investment are the second tier VC’s. These VC will have fund sizes of between £100 and £200m. They have a problem of deployment. They are looking to square the circle of portfolio theory[2] and management costs[3]. Few VCs want to manage more than 20 investments. This means even a relatively small fund of £100m is seeking to invest at least £5m into each company. Very often companies fall beneath the radar because they cannot efficiently utilise this investment in the required time.

Venture Debt

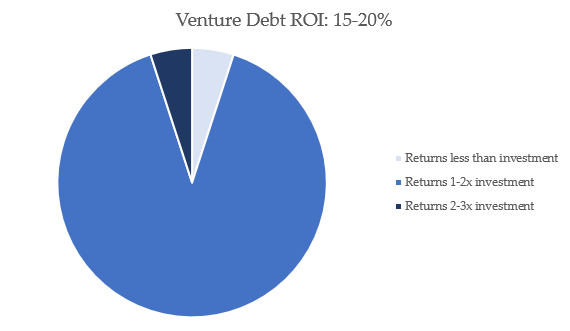

Venture debt investing has a very different philosophy and targeted returns. Firstly, the failure rate is much lower (Runway Growth Capital 2.4%- 8%[4]). This is, firstly, because the criteria of investing (proven revenue model, corporate governance, existing equity investors) acts as an effective pre-screening. Secondly, the reduced need to generate super-normal returns required under the VC model should lead to more prudent decision-making: companies do not need to implement a dash for growth. And thirdly, the range of investible companies and sectors increases. It is not necessary for a company to be in a rapidly growing large market, have an exit strategy, or be a disruptive presence. In the Ruffena model, our target is companies that can grow revenues at 25% per annum plus over the three-year period of our loan.

Note: These returns are indicative and may vary.

The second key aspect of Venture Debt is that it is a yield instrument. Income is generated in a steady and frequent stream of cash. Cash is generated through interest payments and capital repayments. In addition, in the Ruffena model, there is a “Put” option to convert the Warrants to cash at the end of the loan period or retain the warrants to benefit from a company sale or IPO. This model contrasts starkly with the money in-money out VC model which has one liquidity event per investment. The Ruffena model targets an 18% internal rate of return and after losses is expected to achieve 12%.

The Bottom Line

Venture Debt offers investible funds to a wider range of companies than VCs. This is because the business model of venture debt is built on achieving a lower return from each investment. A VC model yields at best an IRR of 12% achieved from many failures and a few successes. This sets the bar very high for investment as each company must potentially be a huge success. Venture Debt offers a much wider range of companies access to investible funds and offers investors an opportunity to benefit from the upside of private company investment, through warrants to purchase equity while increasing the chance of investors getting their money back.

About Ruffena Venture Finance

Ruffena Venture Finance provides venture debt loans between £500,000 and £2million to growth companies. We seek companies that meet the following criteria:

- Have a robust, proven business model

- achieved a solid base of revenue and a strong pipeline of sales showing growth of 25% per annum plus

- a base annual revenue of at least £1m

- a well-researched business plan

- systems for providing monthly business management information

- strong corporate governance including an active chairman and a balanced board

- A full or part time finance director

[1] https://techcrunch.com/2017/06/01/the-meeting-that-showed-me-the-truth-about-vcs

[2] Portfolio theory is an attempt to manage risks by diversifying investments.

[3] VC’s are expected to make a significant contribution to the ongoing management of their investments. This may involve: sitting on the board, advising management, helping raise further funding, recruitment.

[4] David Spreng CEO of Runway Growth Capital, Woodside, California 2019.