Europe’s energy storage startup landscape

For much of the past decade, energy storage has been discussed primarily as an enabling technology for renewable generation. Batteries, in particular, were seen as a necessary complement to wind and solar – important, but largely reactive to upstream developments. Recent investment data suggests that this view is no longer sufficient. Energy storage is now emerging as a strategic layer of Europe’s energy system in its own right.

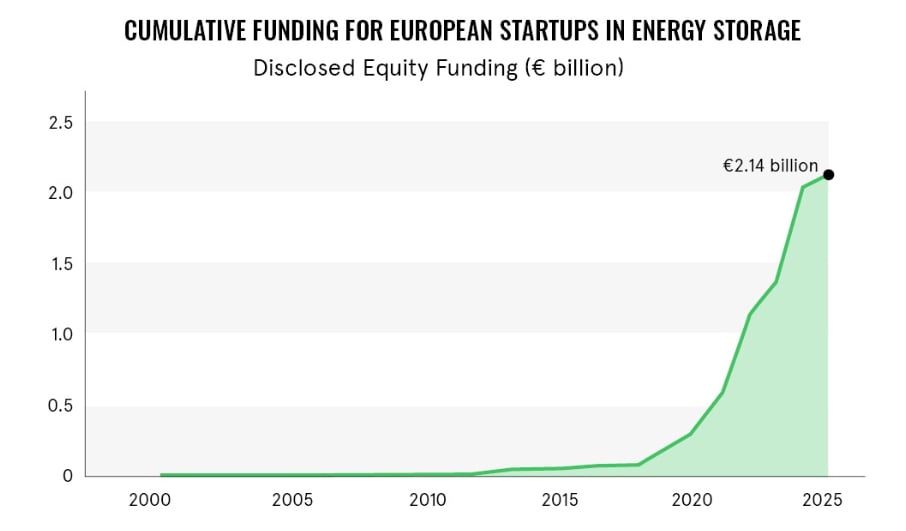

According to new research mapped by Avnet Silica, European startups producing energy storage hardware have raised a total of €2.14 billion in equity funding. Nearly half of that capital has been deployed in the past three years, and more than 80% within the last five. This acceleration points to a market moving into a more structural phase, where deployment, integration, and resilience matter as much as technological novelty.

Battery storage as a baseline, not a frontier

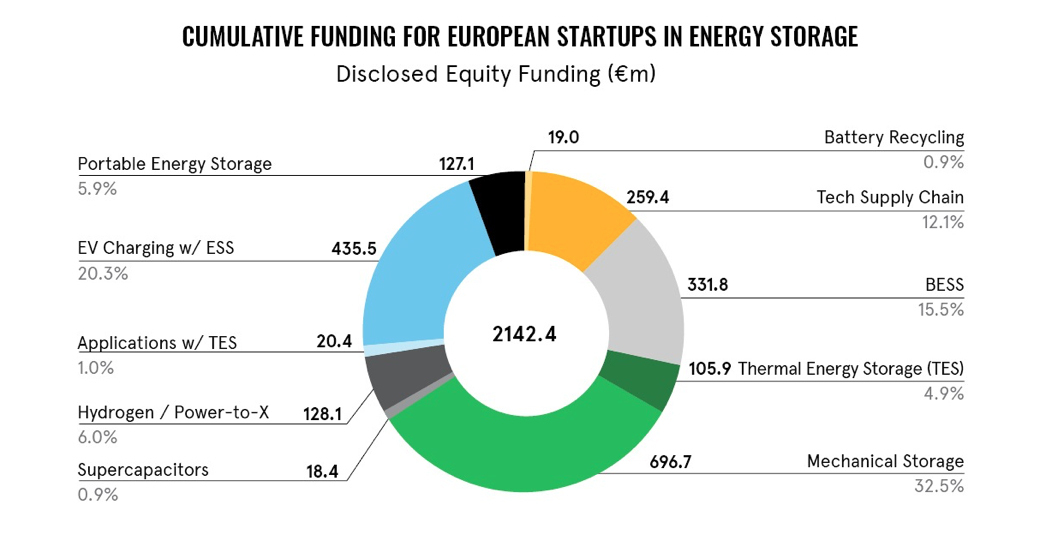

Battery energy storage systems (BESS) continue to be a central pillar of the market, attracting €331.8 million in startup funding. Lithium-based technologies account for the majority of this investment, reflecting their commercial maturity, established supply chains, and proven performance across grid-scale, commercial, and industrial applications.

The more interesting shift lies in how the role of BESS startups is evolving. Our analysis indicates that a significant proportion of European BESS companies are already at or near commercial maturity. These startups are increasingly differentiating through system-level offerings, including turnkey deployment, advanced software for monitoring and optimisation, and lifecycle services such as predictive maintenance, rather than competing solely on chemistry.

In energy storage, this reflects growing customer expectations – particularly among utilities and industrial users. Storage assets are increasingly expected to perform as dependable infrastructure, not experimental add-ons.

Capital flows signal diversification, not fragmentation

While BESS remains foundational, the broader funding landscape shows clear diversification. Mechanical energy storage startups have attracted the largest single share of investment, at nearly €700 million, despite representing a smaller number of companies. Technologies such as gravity-based and liquid air energy storage are capital-intensive, but they address a critical gap: long-duration storage at grid scale.

At the same time, startups combining EV charging with embedded energy storage have raised over €435 million. This convergence represents a practical response to real-world constraints. As electric vehicle adoption accelerates, grid connection limits and peak demand charges increasingly shape infrastructure deployment. Buffered charging solutions allow power to be stored off-peak and delivered rapidly when needed, decoupling charging performance from instantaneous grid capacity.

Thermal Energy Storage (TES) has also gained traction, securing more than €100 million in funding. Unlike electrochemical storage, TES targets industrial heat – one of the more challenging aspects of decarbonisation. Investment in this segment suggests a growing recognition that energy storage must address not only electricity, but the broader energy system.

Collectively, we find that these trends suggest the market is broadening rather than fragmenting. Different storage technologies are being developed to solve different problems, from grid stability and transport electrification to industrial heat and long-duration balancing.

Innovation shifts to the system level

Innovation is increasingly centred at the system level. Across BESS and adjacent segments, many startups emphasise software capabilities, hybrid architectures, and sustainability credentials alongside hardware performance. This marks a shift away from component-centric innovation toward system optimisation.

In practical terms, this means storage solutions that are easier to deploy, integrate, and manage at scale. Digital layers enable operators to extract more value from installed assets, while sustainability considerations – such as recyclability, second-life batteries, or lower-carbon manufacturing – are becoming part of competitive positioning rather than peripheral claims.

Importantly, a parallel stream of investment is flowing into the energy storage supply chain itself. More than €250 million has been directed toward next-generation battery chemistry, diagnostics, and cell or module production. This suggests that investors are not only backing end-use systems, but also seeking to strengthen Europe’s industrial base and reduce exposure to concentrated global supply chains.

Strategic implications for Europe’s energy transition

Taken together, these patterns point to a sector entering its structural phase. Energy storage is increasingly understood as a portfolio of solutions underpinning grid resilience, industrial electrification, and energy security.

For policymakers, this shift raises important considerations. Supporting deployment frameworks, grid access, and market mechanisms may now be as impactful as funding early-stage research. For industry stakeholders, the data highlights the importance of interoperability, standards, and integration across energy vectors. Crucially, while competition is intensifying, the market remains open. The diversity of funded technologies suggests that Europe’s energy transition will not hinge on a single breakthrough, but on the coordinated deployment of multiple storage approaches – each optimised for a specific role within an increasingly complex energy system.

The next phase of growth will be defined by deployment at scale, not by proving the technology itself. Investment patterns suggest energy storage is moving into the core of Europe’s decarbonisation strategy, becoming part of the system architecture itself. Startups are helping shape how energy is stored, moved, and used in the decades ahead.